Want to hear some good news about mortgage rates that involves them being a lot higher than they previously were?

Yes, I know that sounds absurd, but hear me out. There are now millions more mortgages that feature rates above 6.5%, and many with rates above 7%.

There are also millions less that feature rates below 5% than there were just a couple years ago.

Why is this good you ask? Well, it means the effects of mortgage rate lock-in are beginning to wane.

It also means millions of borrowers might stand to benefit from a refinance is rates eventually drop.

Nearly a Quarter of Mortgage Holders Have an Interest Rate Above 5%

The latest Mortgage Monitor report from ICE released this week found that there’s been quite a shift in outstanding mortgage rates.

While it was quite common for a homeowner to hold a 30-year fixed priced at 2-3% a few years ago, it’s becoming less so today.

In fact, as of May some 24% of those with outstanding home loans had a mortgage rate at or above 5%, up from just 10% two years ago.

At the same time, there were there nearly six million (5.8M) fewer mortgages with rates below 5% than there were just two years ago.

And nearly five million (4.8M) fewer with rates below 4%, thanks to borrowers either selling their homes or in some cases pursuing a cash out refinance.

While the low-rate homeowners shed their mortgages via home sale or refinance, a new batch of high-rate homeowners is beginning to take their place.

Since 2022, four million new 30-year fixed mortgages have been originated with rates above 6.5%, and of those roughly half (1.9M) have rates north of 7%.

In other words, the collective outstanding mortgage rate of all homeowners is rising.

This means it’s becoming less normal to have an ultra-low interest rate and that could mean fewer roadblocks when it comes to selling and increasing for-sale inventory.

Why Is This Good Exactly?

In a nutshell, the shift from loose monetary policy to tight Fed policy in the matter of just a year and change wreaked havoc on mortgage rates and the housing market.

We went from 3% 30-year fixed mortgage rates in early 2022 to a rate above 8% by late 2023.

While the Fed doesn’t control mortgage rates, they made a big splash after announcing an end to their mortgage-backed securities (MBS) buying program known as Quantitative Easing (QE).

That meant the Fed was no longer a buyer of mortgages, which immediately lowered their value and raised the interest rate demanded by other investors to buy them.

At the same time, the Fed raised its own fed funds rate 11 times from near-zero to a target range of 5.25% to 5.50%.

While this was arguably necessary to cool off demand in the too-hot housing market, it created a group of haves and have nots.

The homeowners with 2-4% mortgages fixed for the next 30 years, and renters facing exorbitant asking prices and 7-8% mortgage rates.

This dichotomy isn’t good for the housing market. It doesn’t allow people to move up or move down, or for new entrants to get into the market.

Due to the quick divergence in rates for the haves and have nots, home sales have plummeted.

The same is true of refinances, especially rate and term refis, hurting lots of banks and mortgage lenders in the process.

But as the average outstanding mortgage rate climbs higher, there will be a lot more activity in the real estate and mortgage markets.

Here Comes the Refis (Well, Not Just Yet…)

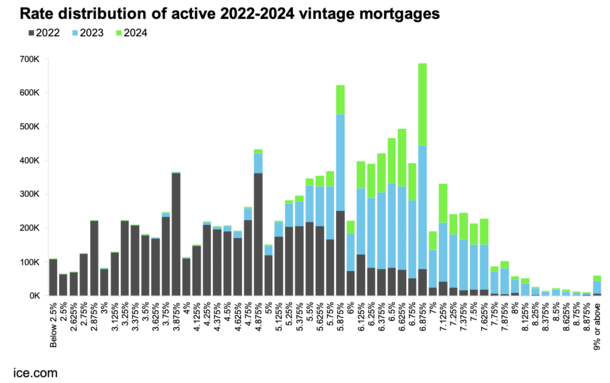

If you look at the chart above, you’ll see that recent vintages of mortgages were dominated by high-rate mortgages.

The distribution of home loans with mortgage rates above 6% surged in 2023 and 2024 as the 30-year fixed ascended to its highest levels in decades.

While this has clearly dampened housing affordability, and led to numerous mortgage layoffs, it’s likely going to be a cyclical challenge that improves each year.

Over time, the low-rate mortgages will be replaced by higher-rate loans. And if mortgage rates moderate as inflation cools, many millions will be in the money a for a refinance.

So aside from mortgage rate lock-in easing and more homes coming to market, which pays off the underlying loans, we’ll also see more refinance activity as recent home buyers take advantage of lower rates.

In fact, we’ve already seen it as the 30-year fixed is roughly 1% below its October 2023 peak, thanks in part to normalizing mortgage spreads.

Those who timed their home purchase badly (in terms of that mortgage rate peak) have already been able to refinance into a lower monthly payment.

And if rates continue to come down this year and next, as is widely expected, we’re going to see a lot more borrowers refinance their mortgages.

This will benefit these homeowners and the mortgage industry, which traditionally relies upon refinances to keep up volume.

So while times have been bleak these last couple years, it’s all part of the process.

The shift out of cheap money and back into reality should get things moving again, whether it’s an uptick in home sales, mortgage lending, or both.